Book a free demo

Oops! Something went wrong while submitting the form.

February 25, 2025

Every swipe, tap, and digital payment at your restaurant is the final touchpoint in your customer's dining experience. However, many restaurant owners find it difficult to navigate the world of payment processing due to the complex menu of fees, terms, and technical requirements.

According to a report by the National Restaurants Association, Canadian restaurants process about 70% of their transactions through credit cards, representing thousands of dollars in daily revenue.

Your choice of payment processor directly impacts your restaurant's bottom line. Many restaurant owners lose 2.5% to 4% of their revenue to payment processing fees, often due to suboptimal processor selection.

With tight profit margins in the food service industry, selecting the right payment processing solution can mean the difference between watching your profits disappear in fees and maintaining a healthy cash flow supporting your growth.

This guide will explain everything you need to know about choosing the right payment processor for your restaurant.

From understanding basic terminology to evaluating security features, we'll help you make an informed decision that will serve your business today and support your growth tomorrow.

Before selecting a processor, it's essential to understand how payment processing works and the key terms involved. This knowledge will help you make informed decisions and negotiate better terms for your restaurant.

Payment processing in restaurants comes with a vocabulary that might initially seem overwhelming.

Let’s have a look at them.

When a customer pays by card at your restaurant, you hear terms like "merchant account," which is your business's bank account for accepting card payments.

The "payment gateway" is the digital bridge between your point-of-sale system and the payment processor, ensuring secure transaction routing.

Another term you frequently encounter is "interchange fees." These are the base rates set by card networks that every processor must pay.

Understanding these fees is vital because they form the foundation of your processing costs.

You will also encounter the term "chargeback." It occurs when a customer disputes a transaction, reversing payment and additional fees for your restaurant.

A credit card payment journey through your restaurant's system is faster than preparing a cup of coffee, yet it involves multiple steps and players.

This entire process typically takes just seconds, thanks to modern technology.

However, the speed and reliability of this process depend heavily on your chosen payment processor and its technology infrastructure.

With iOrders integrated payments, these transactions are streamlined and integrated seamlessly with your existing operations, reducing the chance of errors and saving valuable time during busy service hours.

Your payment gateway needs to work smoothly with your digital ordering system for online orders.

With iOrders' website and QR Ordering feature, you can ensure that customer payment experiences remain smooth and secure, whether they dine in or order takeout.

The complexity of payment processing might seem tough, but understanding these basics puts you in a stronger position to evaluate different processors.

Now, let's discuss various entities involved in processing your restaurant's payments and how they work together to complete each transaction.

Every time a customer pays at your restaurant, a well-orchestrated dance of different organizations works behind the scenes to complete the transaction.

Understanding these key players helps you make better decisions about your payment processing setup.

When diners pull out their credit cards to pay for their meals, they initiate a complex process as cardholders. They might not realize it, but their simple tapping or swiping triggers automated communications between multiple financial institutions.

Their bank, known as the issuing bank, has already verified their creditworthiness and set spending limits that help protect both the customer and your restaurant from fraudulent transactions.

As a merchant, your restaurant is the starting point of the payment journey. Your responsibility includes maintaining secure payment terminals, training staff on proper payment handling, and ensuring your systems meet security standards.

Modern payment solutions, like those integrated with iOrders, can help you track these transactions while gathering valuable customer feedback. Thus, each payment interaction becomes an opportunity for business improvement.

Credit card networks like Visa and Mastercard set the standards for how transactions flow through their systems. They work closely with payment processors, who handle the actual movement of money between banks.

Your processor acts as your primary point of contact, managing everything from transaction routing to dispute resolution.

Two types of banks play essential roles in every transaction.

The issuing bank (your customer's bank) verifies the cardholder's ability to pay and approves the transaction.

While the acquiring bank (your restaurant's bank) receives the payment and deposits it into your merchant account.

The payment gateway acts as a secure tunnel for transaction data.

It is the digital version of an armored car, protecting sensitive payment information as it travels between different entities. The gateway encrypts card data, verifies transaction details, and helps prevent fraud.

Now that we know the key players in payment processing let's explore the specific features you should consider when choosing a payment processor for your restaurant.

Selecting the right payment processor for your restaurant requires careful evaluation of several key features.

Your choice affects everything from daily operations to long-term growth potential, so investing time to understand these elements is important.

Here are the features you must consider when choosing credit card processing for your restaurants.

In the fast-paced restaurant environment, every second counts. Your payment processor must complete transactions quickly and consistently, especially during peak hours.

Modern processors should complete most transactions in under three seconds, allowing your staff to serve more customers efficiently.

However, speed shouldn't come at the expense of reliability - your system needs to maintain performance even during high-volume periods.

A reliable processor also provides backup processing methods when internet connectivity fails. These include offline processing capabilities or cellular backup systems.

When integrated with comprehensive solutions like iOrders's Online Ordering System, these backup features ensure you never have to turn away a paying customer.

Payment security isn't just about protecting card data - it's about safeguarding your restaurant's reputation.

Look for processors that offer end-to-end encryption, which protects customers until the transaction is complete.

Tokenization adds another layer of security by replacing sensitive card data with unique identification symbols, making it useless to potential thieves.

The best processors also provide fraud detection tools to identify real-time suspicious transactions.

These systems work alongside your online ordering to help spot potential issues before they become problems, protecting you and your customers.

Your payment processor should integrate seamlessly with your existing restaurant management systems, including your point-of-sale system, accounting software, and digital ordering platforms.

The right processor will also integrate smoothly with services like your website and QR Ordering, allowing you to manage all your transactions from a single dashboard.

Modern processors should also support various payment methods, from traditional cards to digital wallets and contactless payments.

This flexibility helps you serve customers who prefer different payment options while preparing your business for future payment technologies.

Even the best systems occasionally need support, and that's when the quality of your processor's customer service becomes invaluable.

Look for processors that offer 24/7 support through multiple channels - phone, email, and chat. Their support team should understand the unique challenges of restaurant operations and be able to resolve issues quickly.

Consider reading user reviews from other restaurant owners, particularly about their experiences with customer support during busy periods or emergencies.

A processor's response during these moments often reveals their true value as a business partner.

Now that we've covered the essential features let's examine the various rates and fees you must pay the payment processor.

Understanding the cost structure of payment processing is essential for effectively managing your restaurant's finances.

While the terminology might seem complex, overviewing these charges before signing up can help you make informed decisions about your payment processing partner.

Most processors charge a monthly fee to maintain your merchant account and provide basic services. These charges cover account maintenance, statement generation, and access to the processor's support services.

While some processors advertise "no monthly fee" plans, they often compensate for this by charging higher per-transaction rates.

A monthly fee is like a membership cost. It provides clear value through better rates or additional services.

Some processors charge monthly fees for extra features, such as advanced reporting tools or integration with restaurant management systems.

Processing fees come in several forms, with interchange-plus pricing being the most transparent. Under this model, you pay the card network's interchange rate plus a fixed markup.

For example, if the interchange rate is 1.5% and your processor's markup is 0.3%, you'll pay 1.8% per transaction. This clarity helps you understand what you're paying for.

While flat-rate pricing is simpler, it often costs more in the long run. Some processors charge different rates for card-present versus card-not-present transactions, which becomes particularly important when handling in-person dining and online orders.

Beyond regular processing fees, you might encounter various situational charges.

Chargeback fees occur when customers dispute transactions, while batch processing fees apply to daily settlements. Some processors also charge for payment gateway access or PCI compliance support.

Watch out for processors that charge early termination fees or equipment restocking fees. If you're not careful, these hidden costs can add up quickly.

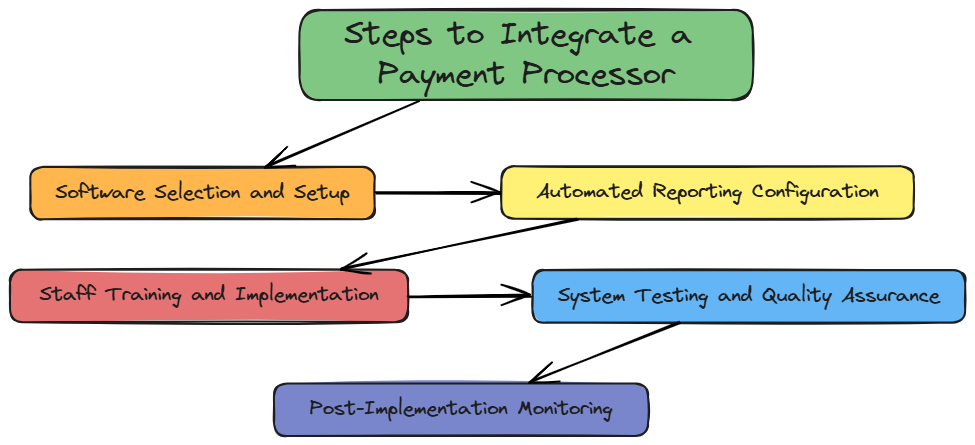

Now that we have a brief idea about the fee structure let's explore how to properly integrate a payment processor into your restaurant's operations to ensure a smooth transition and minimal disruption to your business.

Implementing a new payment processor requires careful planning and execution. A well-thought-out integration process ensures smooth operations and minimizes disruptions to your daily service.

You can integrate a credit card payment processor using the following steps:

Your payment processing system must work harmoniously with your existing restaurant management software.

Begin by confirming compatibility with your current point-of-sale system and other essential tools. Many modern processors offer plug-and-play solutions, but you'll want to verify that all features function properly with your setup.

Integration becomes notably smoother when working with comprehensive platforms. iOrders's White-label Native Mobile App already includes built-in payment processing capabilities that sync seamlessly with your existing systems.

This integration ensures consistent performance across all ordering channels, from in-person dining to online orders.

Setting up your reporting systems can save you countless hours of manual work later. Modern payment processors offer detailed analytics that tracks transaction patterns, peak business hours, and popular payment methods.

Configure these reports to generate and distribute to relevant team members automatically.

You can track the success of promotional offers, understand customer spending patterns, and adjust your marketing strategies accordingly. This data-driven approach helps you decide about menu pricing and promotional strategy.

Your team needs thorough training on the new payment system to ensure smooth operations.

Create a comprehensive training schedule that covers basic transaction processing, troubleshooting common issues, and handling special cases like refunds or split checks.

Consider designating "power users" who can assist others during the transition period. Include specific training on security protocols and fraud prevention.

Your staff should understand how to spot suspicious transactions and know the proper procedures for handling sensitive payment information.

This knowledge becomes especially important when managing in-person and digital payments through integrated systems.

Before going live, conduct thorough testing of all payment scenarios. It includes processing various payment types, handling refunds, splitting checks, and managing high-volume situations.

You must also test your backup systems to ensure business continuity during internet outages or other technical issues. Document any problems and work with your processor's support team to resolve them promptly.

Run parallel systems during the initial transition period. It provides a safety net while your team becomes comfortable with the new processor.

After launch, closely monitor system performance and gather feedback from staff and customers. Look for patterns in transaction issues or customer complaints.

Regular monitoring helps you identify and address problems before they affect your business operations.

Understanding the technical aspects of payment processing integration is important, but ensuring your system meets all security and compliance requirements is equally crucial.

Let's explore these security and compliance requirements in the next section.

Protecting your customer’s payment data is essential for your restaurant's reputation and legal standing.

Thus, your payment processing system should guard sensitive financial information, making security and compliance fundamental to your operations.

Payment security starts with strong encryption.

When a customer hands over their credit card at your restaurant, the data needs protection. Modern encryption transforms card numbers into unreadable code, making them useless to potential thieves.

Tokenization adds another layer of protection by replacing actual card numbers with unique tokens. It gives each transaction a special code that only your payment processor can understand.

It means that even if someone manages to intercept the data, they won't be able to use it.

The real card information stays safely locked away in a secure vault while these tokens handle the day-to-day transaction needs.

Another acronym to remember is the Payment Card Industry Data Security Standard (PCI DSS). It's your roadmap to maintaining payment security.

These standards outline specific requirements your restaurant must follow to protect cardholder data. It includes regular security assessments, maintaining secure networks, and implementing strong access control measures.

Following PCI DSS guidelines helps protect your business from data breaches and costly non-compliance fines.

Although the requirements might initially seem overwhelming, many modern payment processors include PCI compliance support in their service packages.

Your restaurant's payment network needs strong boundaries. Firewalls act as security guards, monitoring incoming and outgoing network traffic and blocking suspicious activities.

It separates your payment system from other parts of your business network, creating a secure environment for payment processing.

Access controls determine who can view and handle sensitive payment information. Proper user permissions ensure that only authorized staff members can access specific parts of your payment system.

It becomes important in restaurants where multiple servers handle transactions throughout the day.

These security measures help maintain their effectiveness through regular monitoring and updates.

With iOrders's White-label Native Mobile App, you get built-in security features that integrate with your existing firewall and access control systems. These features provide an extra layer of protection for in-person and online transactions.

As you strengthen your restaurant's payment security, remember that technology and threats constantly evolve.

Let's discuss how to avoid common pitfalls impacting your payment processing success.

Minor oversights can lead to significant financial and operational challenges when selecting a payment processor for your restaurant.

Understanding these potential pitfalls can help you make informed decisions that will benefit your business in the long run.

Payment processing contracts often come with enticing introductory rates that mask long-term commitments.

Before signing, examine the contract duration and understand what happens after the promotional period ends. Many restaurants are locked into unfavorable terms because they didn't anticipate rate increases or changing business needs.

Your business needs may change, especially as you expand your service offerings or adapt to market conditions. A contract that seems perfect today might become restrictive as your restaurant grows.

Payment processors often bundle their core services with additional features you might not need.

While these extras might sound appealing during the sales pitch, they can significantly increase your monthly costs. Take time to evaluate which services truly benefit your restaurant's operations.

Consider whether features like advanced reporting tools or specialized hardware align with your current needs.

Some processors include mandatory add-ons that don't integrate well with your existing systems.

Equipment leasing arrangements often appear cost-effective initially but can become expensive over time.

Many restaurants don't realize they'll pay several times the equipment's actual value through monthly lease payments. Some processors require proprietary equipment that limits your ability to switch providers or upgrade systems.

Buying payment processing equipment outright usually proves more economical in the long run.

Modern solutions, like iOrders, reduce your reliance on traditional payment terminals while providing secure, efficient payment options for your customers.

Let's conclude our discussion on selecting the right payment processor for your restaurant's unique needs.

Choosing the right payment processor impacts every aspect of your restaurant's operations, from daily transactions to long-term growth.

As you evaluate your options, remember that the best choice aligns with your current needs and future business goals.

Your payment processing decision affects your staff's efficiency, customer satisfaction, and bottom line.

Consider how each potential processor handles transaction speeds during peak hours, provides technical support when issues arise, and adapts to changing payment technologies.

Remember that the lowest rates don't always indicate the best value—factor in the quality of service, integration capabilities, and system scalability.

Mobile payments, contactless transactions, and online ordering have become standard expectations for many diners.

Your processor should handle these payment methods seamlessly while preparing for future innovations in restaurant payment technology.

Ready to Streamline Your Restaurant's Payment Processing?

At iOrders, we understand the complexities of restaurant payment processing. Their comprehensive suite of solutions works seamlessly with leading payment processors, creating a smooth and secure payment experience.

Contact iOrders us today for a consultation to learn how we can help optimize your restaurant's payment processing and overall operations.

.png)